|

Underlying Process

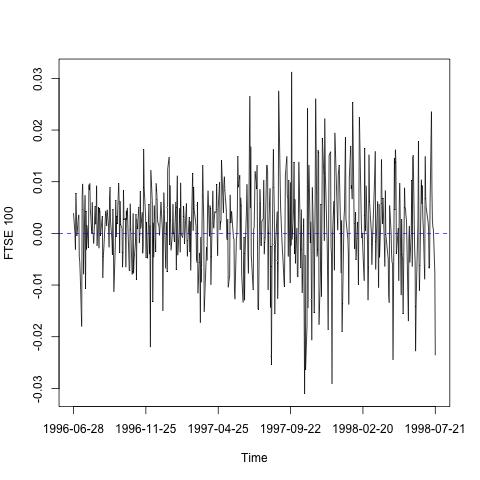

IThe statement `process thought to underly the series' is a model statement. For the FTSE100 data, nobody knows, what process, if any, actually underlys and generates the FTSE data. However, we can formulate a model that we think is appropriate for this data and such a model is a commonly held assumption about the data. For example, we might assume that the model mean is exactly zero. One could, if one wished, choose another model, e.g. one where the mean is precisely 0.000935. That model might fit this data set better, but analysis of many other similar series, or even future observations of this series, might show means that were slightly positive and some slightly negative so that, overall, a mean zero model is typical. An aim of statistics, including time series analysis, is to choose simple models that fit the data well.

Stationary Time Series

Loosely speaking, a stationary time series is one whose statistical properties are constant over time. What do we mean by statistical properties? We mean things like mean value (or average level) of the series, the variance (variation of the time series around the mean level) and the autocorrelation (explained later). One might consider the FTSE 100 time series (above) to be appropriately modeled by a stationary model, but almost certainly the measles series which we exhibit next, is not.

Measles...

|

|